Key takeaways from our Chicago Revenue Cycle Summit

- Eric Fontana

- Mar 17

- 7 min read

The Union Healthcare Insight research team recently got together in Chicago with an experienced group of health system leaders, technologists, and consultants to dig into some of our latest research: “Six insights for revenue cycle leaders in 2026”. It was an open and generative day of discussion where attendees had the chance to sit with some hard questions facing the industry, knock around some practical ideas for moving the needle on their most stubborn challenges, and engage in a mature exchange of diverse perspectives (that didn’t always align). A great day, and many thanks to all involved.

If you’d like a glimpse of the material we discussed, we'll be presenting a slice of this content as part of our Board Briefing series on Thursday, March 26, from 1-2 p.m. ET. Click here to register. You can also view the full list of strategy and revenue cycle summits coming later this year if you’d like to experience a full day of discussion with industry peers and contemporaries. And of course, we’re also happy to bring this material to you directly. If that’s of interest, please reach out at info@unionhealthcareinsight.com.

Here are the major themes that emerged over the course of our discussion:

1. The transformation of health system revenue cycles into a strategic pillar—and the implications of that shift

The summit group broadly agreed that the revenue cycle must move away from its historical identity as a back-office cost center to a key strategic driver for health systems. Regardless of how we came to view revenue cycle as adjunctive to core strategy, the financial stakes are now too high and the external environment is now too unforgiving for that old posture. Payer mix, and the dynamics of the underlying subpopulations, have meaningfully shifted:

Medicaid reimbursement is being pressured from federal budget maneuvers.

Medicare Advantage has become a thorny situation reimbursement-wise.

Profitable procedures are now at greater risk for outpatient migration.

Patient affordability concerns are continually rising.

Technology and data is more pivotal than ever, and payers are using “shape-shifting” tactics (effectively diversifying their playbook to counter enhanced provider response) as they navigate rising MLRs and other forms of business pressure.

Elevating revenue cycle to a genuine strategic pillar means agreeing to make the necessary investment in technology and talent. It also means that the most senior C-suite executives engaging with payer contract strategy as actively as they do with growth strategies such as service line planning. And it means establishing governance structures that move well beyond VP-level accountability toward Chief Revenue Officer roles with actual enterprise authority and scope of practice befitting the title of “Chief”. Participants also highlighted the recognition of some common, thematically related gaps, including how boards often underappreciate revenue cycle risk, how rarely payer performance data informs growth planning, and how revenue cycle leadership is often not in the room when financial strategy gets set.

In essence, we’re talking about a fundamental reorientation of how revenue cycle leadership is routinely folded into strategy and operations. But systems do seem to be recognizing the level of urgency: It’s no coincidence that many of the not-for-profit health system presentations at the JP Morgan Healthcare conference earlier this year gave stark nods to the “re-envisioning or “renewal” of revenue cycles as a recurrent theme (albeit one that much post-conference reporting overlooked, preferring to focus on shiny AI hype train narratives).

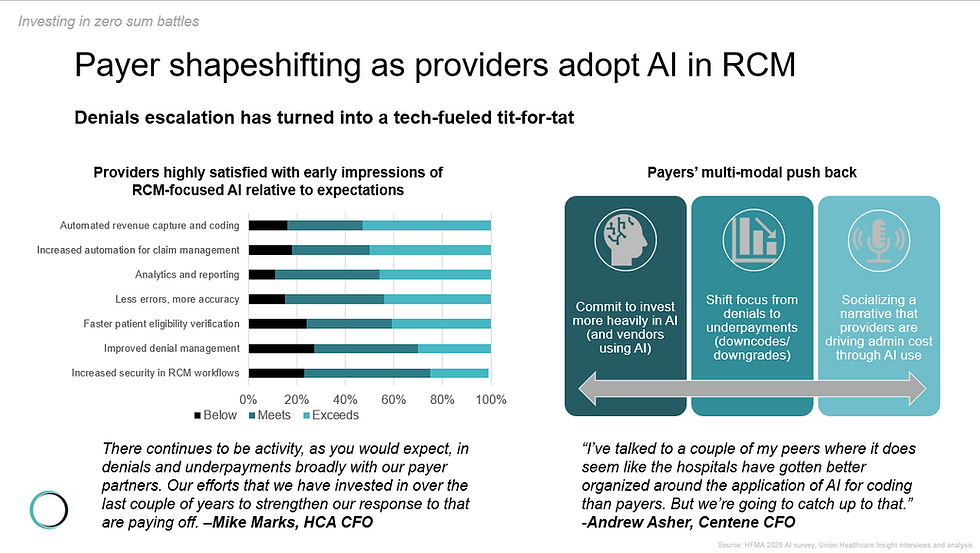

2. AI is leveling the playing field for some while tilting it for others—and there is no sustainable fix to payer-provider friction on the horizon.

Payer-provider friction (escalated by AI use on both sides) was perhaps the dominant theme of our group’s discussion. The health systems that count themselves as early adopters are undoubtedly seeing renewed hope when it comes to fighting back against what one health system contracting leader described as a “Niagara Falls” of denials.

The group recognized that the challenges seen in late 2024 and throughout 2025 were effectively the tail-end of “Phase 1” of AI in the payment/revenue integrity battle. “Phase 2” sees payers diversifying their playbook to include underpayment and auto downgrades, a set of tactics that are harder for providers to immediately identify and quantify (revealing limitations of traditional RCM benchmarking) and therefore directly counter with the methods they perfected in the mid-2010s.

Our discussion of AI's role in revenue cycle management surfaced a tension that we’ve seen play out repeatedly in health care: a growing divide between the haves and have-nots. Sophisticated health systems with mature data infrastructure and the capital to invest in advanced tools are likely to pull ahead, accelerating clean claim rates, shrinking denial lag, and converting prior authorization workflows from reactive firefighting into predictive defense. On the flipside, for smaller health systems, the AI wave is compounding disadvantage, particularly for those reeling from the initial challenges posed by OBBBA with already limited resources. Those forced to rely on legacy platforms and heavier manual workflows, are finding themselves outgunned. The emerging asymmetry positions AI as both a lifeline and a liability, depending entirely on which side of the capability gap a health system sits. That has real consequences for organizations, not to mention the communities they support.

Meanwhile, regulatory scaffolding designed to rebalance payer-provider dynamics remains limited, containing enough enforcement gaps to make it more likely we see at least some of the intended impact be creatively side-stepped.

Summit participants converged on an uncomfortable conclusion: The friction embedded in today's payer-provider relationship is not a technical problem awaiting a smarter solution—it is a structural and economic feature of the system, one that AI appears more likely to intensify than resolve in the near term.

3. The labor outlook for revenue cycle is genuinely uncertain, and health systems are taking a variety of approaches to future planning.

Unlike the broader tech industry, where we’ve seen numerous reported examples of AI-attributed layoffs, healthcare, particularly the revenue cycle, has remained largely immune to such narratives. Most recent administrative staff layoffs have very clearly been linked directly to margin performance. And yet, while the “enabling our teams to do more” mantra is oft uttered by many revenue cycle leaders today, there appears to be a (quiet) acknowledgement brewing in pockets of the industry that emerging agentic AI adoption could swing the proverbial pendulum on this discussion. How far and how fast is anyone’s guess, but near-term layoffs at scale shouldn’t be automatically assumed. Health systems will be contending with several forces, some seemingly at odds with others:

Health system’s critical place as an expected key employer—of humans—in communities across the country.

Pressing margin preservation and growth imperatives.

The recognition that many aspects of the revenue cycle remain manual in nature (though the manner and nature of the manual work may shift markedly as automated capabilities advance).

The possibility that AI could reveal new opportunities requiring additional human resources.

Our discussion highlighted examples of provider organizations that are actively planning for future shifts, including early moves to accommodate agent-inflected workflows—not only with a different staff profile, but a wholesale reframing of what type of professional skills might be required to drive future success. These are murky waters for revenue cycle leadership. But we’re starting to see some forward thinkers position themselves to re-envision their teams as new technology emerges on the horizon.

4. Revenue cycle performance data is a strategic asset that most health systems aren’t close to fully leveraging.

One of the summit's sharpest recurring themes was the gap between what revenue cycle data contains and what most health systems do with it. Denial rates, payer-specific adjudication patterns, CARC/RARC trending, underpayment frequency by contract tier, and clean claim performance by service line represents something far more consequential than operational scorecards—they constitute a real-time intelligence feed on payer behavior, contract integrity, and ultimately, negotiating leverage. Yet, for many, the dominant organizational posture remains reactive or perhaps more concerningly sits in the “problem admiration” phase (an open concern some revenue cycle leaders have proactively surfaced, particularly around regional/geographic score-carding efforts), living inside systems and databases rather than making its way to the C-suite in a form that drives modified ground-game in payer engagement. Summit participants examined what it looks like when health systems flip this dynamic—using denial pattern analytics to expose bad-faith payer conduct before contract renewal, deploying underpayment trending as evidence when in direct discussions with payers, and building a robust evidence base to confront payers on practices that are not compliant with their own policies. The conversation made clear that there is opportunity to improve interactions between providers and payers, particularly when adjudication data is leveraged as a decisive piece of insight (a concept coined: “Analytics as armament”).

A data-driven tactical ground game likely represents health systems’ best hope in payer-friction interactions, at least for now, as the broader system searches for a sustainable equilibrium, however that may ultimately be accomplished. Our group discussed some of the emerging solutions and ideas in the marketplace that promise a more direct connection between payers and providers via APIs. Nevertheless, skepticism abounds that the current incentive structures will allow any technology to meaningfully overcome current obstacles. Said differently, it’s not a technology barrier, but a lack of clear business models that prevents the pursuit of meaningful advancement when it comes to simply connecting both ends of the technology pipes together.

5. Revenue cycle strategy must be in aid of a key mission: Supporting communities to put patients at the core

While items 1-4 in this recap might risk reading like a wide-ranging discussion of strategic and tactical moats—and make no mistake health systems do need to guard against revenue erosion—the pursuit of stronger margins ultimately positions health systems to strengthen support for community health wherever possible. That perspective resonated throughout our research. Few would argue that OBBBA will play a role in reducing access for at least some of the neediest, which hits particularly hard given already pressing affordability concerns that are already forcing trade-offs between essential basics: food, housing, utilities and healthcare.

The group discussed emerging approaches where health systems can improve their existing financial and navigational support for patients. One point for optimism is emerging technology and data assets that can aid in identifying patients who may be “at-risk” and then facilitating connections to sources of funding. These types of approaches benefit the patient and their families, by reducing barriers to access, and minimizing disruption to initiation (and continuation) of treatment. Such applications of AI and tech are often less newsworthy than their “battle-it-out” payer vs provider counterparts. However, they’re equally (if not more) important, given the critical role health systems play in supporting their communities’ health and well-being.

Want to join a future Revenue Cycle Summit? Contact us here: Check our registration page for future strategy and revenue cycle focused events.